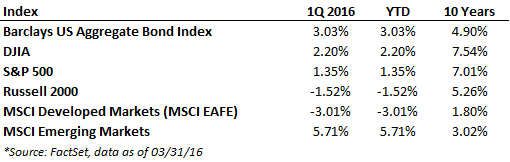

The S&P 500 recovered sharply to close the quarter up 1.35%, despite falling over 10% through mid-February. The V-shaped recovery in the stock market underscored the heightened volatility seen during the first quarter. Things got off to a rocky start as the S&P 500 and the Dow posted their worst ever year-opening weeks as the markets continued to digest the mid-December rate hike and declining oil prices. There were concerns that a slowing global economy might be dragging down the U.S., which weighed heavily on market sentiment and growth expectations. However, the clouds soon parted and the market gains seen in the second half of the quarter more than compensated for the initial sharp decline.

In the first few weeks of the year, investors reacted negatively to poor manufacturing data out of China and slowing demand for U.S. exports. This was confirmed by the lowest level of Purchasing Managers Index (PMI) of U.S. manufacturing activity since 2009, durable goods orders falling, weakening retail sales data and a significant slowdown in January payroll growth. Added to the disappointing economic data, oil hit a 13-year low on February 11 following a supply surge and data showing production continued to outpace demand.

What was starting to look like a rout turned when news surfaced that OPEC members might agree to an output freeze. Though this has yet to occur, oil prices rallied and pulled the stock market up with them. This was followed by improved U.S. economic data later in the quarter, and the market was no doubt supported by the more dovish Fed rhetoric through the end of March. When the Federal Reserve Board raised rates in December Fed Chairwoman Janet Yellen suggested there were four rate hikes coming in 2016. Many chose to suspect March would be the first of those. When the Fed did nothing and stated it would “proceed cautiously” the stock market found a second catalyst to advance.

In fixed income markets, intermediate and long-term treasury yields sharply declined during the quarter, as safe-haven assets benefitted from risk aversion at the beginning of the year and a softening in the Fed’s stance after the December rate hike. The 10-year yield fell from 2.27% at the end of December to 1.77% at the end of March, a sharp move that certainly caught some investors by surprise. High-yield and emerging markets debt also saw gains for the quarter, especially in the second half as a dovish Fed and a rebound in the price of oil encouraged investors to move back into riskier asset classes.

Global markets had mixed results in the first quarter, as international developed markets (MSCI EAFE) were down 3% for the quarter while emerging markets (MSCI EM) rebounded sharply and were up 5.71%. Eurozone equities were negatively impacted by sluggish growth, as GDP grew by only 0.3% in the 4th quarter of 2015 and inflation fell to -0.2% year over year in February, well below the ECB target of 2%. Security concerns continued to dominate the headlines after the Brussels terrorist attacks in March.

Global central banks continued to increase accommodative policies. The Bank of Japan cut its main policy rate to below zero, citing concerns about the impact of volatile global markets on their dampened domestic economy and weak oil prices affecting their inflation target. This was followed by the People’s Bank of China reducing its reserve ratio on banks to 0.5%, the fifth such move in the last year. Then the ECB made a slew of accommodative moves in early March, highlighted by a cut in all three of its key interest rates—most importantly taking its overnight deposit rate further into negative territory at -0.4% in an effort to bolster the euro zone’s weak economy and avoid deflation. Additionally, the ECB agreed to increase its monthly asset purchase program to 80 billion euros per month from 60 billion. ECB head Mario Draghi continues to show that he is not short of tools to combat deflation and stimulate the euro zone economy.

Emerging markets were a bright spot in the first quarter, as EM investors were encouraged by a deferral in expectations of a rate hike in the U.S. and weakening of the U.S. dollar. Latin American equities registered gains with Brazil the strongest market amid expectations of domestic political change, strengthening currency against the dollar, and improvements in commodity prices. A strong gain in Russia occurred on the back of rallying oil prices and strength in the ruble, which rebounded from a record low level against the dollar. Emerging Asian markets were more mixed, as soft economic growth and yuan weakness in China provided a significant headwind. The MSCI Emerging Markets Index actually entered a bull market – defined as a 20% rise from a recent low—during the quarter after the index sharply rallied from its lowest level in six years in January.

In election developments, in the month since we sent out the Karl Rove piece, Mrs. Clinton appears to have locked up the nomination as Mr. Sanders has started laying off campaign workers. On the GOP side of things, Mr. Trump is closing in on the nomination. He won all 5 contests on April 26th and stands to win all of NJ and a good part of CA in early June. Thus, leaving him only a few delegates shy of the required 50%, which he may be able to pick up in the primaries during May. It is still too early to be sure, especially as the delegates are only required to vote the way of the primary results on the first ballot; from the second ballot they are free to vote as they see fit, but it is his nomination to lose.

We expect the election to add volatility to the markets all the way until November. Even if Mr. Trump does wrap up the nomination before the convention, a Trump vs. Clinton campaign would not add stability to Wall Street. A close election, and the possibility that Mr. Trump might win, would create much uncertainty since no one would know what to expect from a Trump Presidency; a Clinton Presidency would be more predictable. We also expect the price of oil to fluctuate going forward. For us, there are too many upstream companies (the explorers and producers) waiting to buy distressed assets and/or waiting for oil to hit $50 to start drilling, and that is not the attitude that exists when true bottoms are reached. Additionally, Iran production continues to ramp up and the OPEC countries never did actually agree to freeze production. We think the worst is over, but expect oil prices to add to volatility for the next couple quarters.

The first quarter was a testament to why it is important to maintain discipline and adhere to your long term investment plan. Had you looked at your statement on Dec. 31 and then March 31 you would not have seen much change, but of course the market was a roller coaster in between those two points. While there was a lot of noise surrounding the sharp decline and ensuing recovery, it is volatile times like these where opportunity is found.